How will Covid-19 impact the present and future of the leasing industry?

Article prepared for the World Leasing Yearbook 2021

Author: Amina Chakchouk, Leasing COO at CODIX

HOW CAN WE PREVENT THE LONG-TERM EFFECTS OF THECOVID-19 PANDEMIC on the expected economic performance linked to the leasing business from the point of view of the lessor and the lessee? How does the crisis affect the implementation of the right to use assets and the applicable requirements in IFRS16? How can a Covid-19 event be considered in the light of IFRS9 impairment? How can the leasing software system be part of the cure, with a ‘Crisis mode’ or ‘COV in Bank’ management that can easily be switched on?

Following the unprecedented crisis that occurred in 2020 linked to the Covid-19 pandemic, the world has changed dramat- ically in a few months. A rare disaster has resulted in a tragically large number of human lives being lost. Business leaders of vari- ous countries have been forced to take decisions that impact all sectors of activity.

As a result, leasing companies have experienced significantly reduced consumer traffic in retail stores and shopping areas, or indefi- nite closures due to quarantine meas- ures and other government directives. General measures have been imposed on banks and financial institutions by many governments to authorise a temporary moratorium for loans/leases, payment holidays or the granting of additional loans.

So how can we prevent the long-term effects of the Covid-19 pandemic on the expected eco- nomic performance linked to the leasing business from the point of view of the lessor and the lessee?

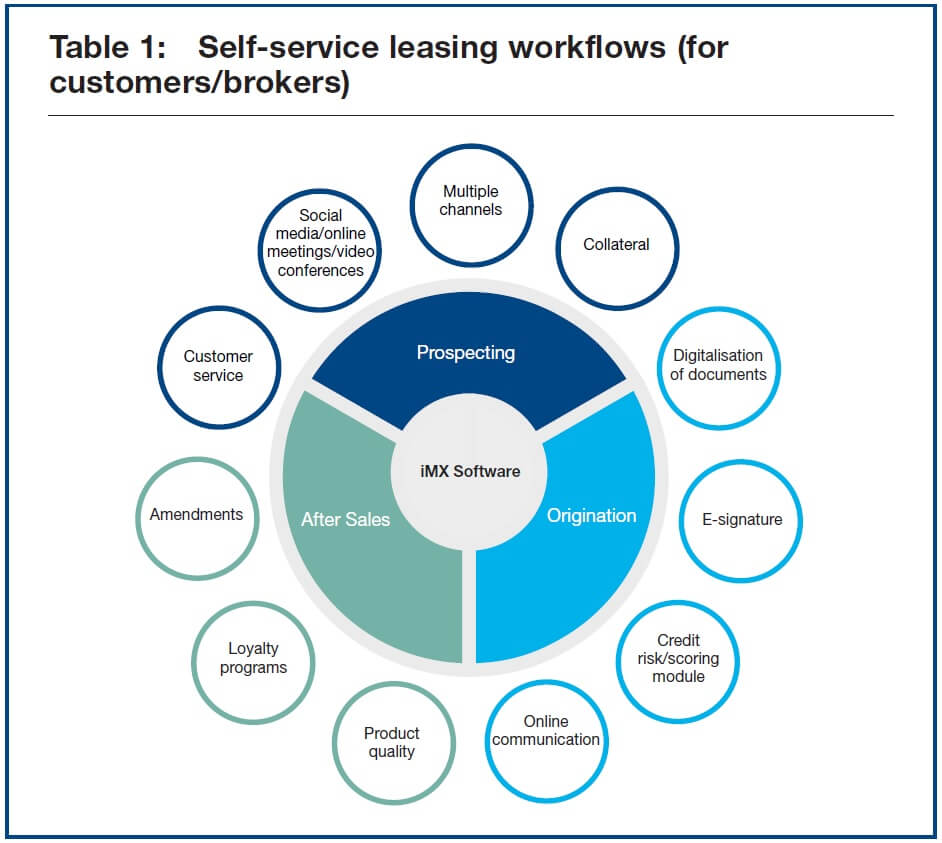

The pandemic and the lockdown have accelerated tendencies in digi- talisation, seeing many leasing/credit finance businesses move their opera- tions entirely online in a short period of time.

The move in this direction is not a new concept for the industry. It becomes more than urgent to accelerate the process of system digitalisation and AI automation to be able to continue and support the fast business change.This can be achieved by put- ting into place leasing software package solutions able to support fully digitalised end-to-end processing with an automated origi- nation/underwriting process, online credit risk decisions, and after-sales automated processes that can easily be parameterised to evolve rapidly as the risk changes.

The risk parameters should be fully set with dynamic criteria that take into account the possible shocks (economic shake out as a result of the pandemic, natural disasters, exchange rate shocks) and adapt automatically to the different processes.

Leasing businesses need to move fast to propose attractive self-service options to their customers, so as to meet customer/prospect needs. Naturally, this means providing web/mobile access that enables cus- tomers to:

- ask to postpone some rental pay- ments, or request payment holi- days;

- add new insurance options, such as ‘natural disaster protection’ or ‘pandemic disease protection’;

- subscribe to new services or switch to pay-per-use services;

- ask to transfer some leasing con- tracts to other lessees;

- automatically extend leasing contracts;

- perform simulations and request amendments to adapt rental pay- ments according to the situa- tion; and

- request the early termination of their contracts.

All this is completed using the latest add-ons technology offers today, such as e-signature, e-identification, document imaging services chatbots, with automating customer notifica- tion services using email/SMS that speed up the processing of workflows.

Presales/marketing professionals will also greatly benefit from more digitalised processes and richer systems by being able to use seamlessly different prospection channels, such as online channels/tele-sales channels/lead/vendor channels.

Adapting the different leasing/credit product settings is nec- essary to protect the business from any other shocks. This trans- lates especially into:

- coming up with new offers, including mandatory banking and government guarantees;

- adapting/amending vendor/dealer/supplier agreements by adding new kinds of guarantees, such as funding guarantees which aim to constitute funding reserves that can be used to cover the customer’s risk of unpaid debts;

- providing mandatory insurances for the different leasing contracts;

- varying the products and the type of assets and performing regular asset valuations to take into account the asset risk that can be impacted by different economic changes; and

- building an automatic refurbishment module to put as quickly as possible an off-lease asset on the market.

How does the crisis affect the implementation of the right to use assets and the applicable requirements in IFRS16?

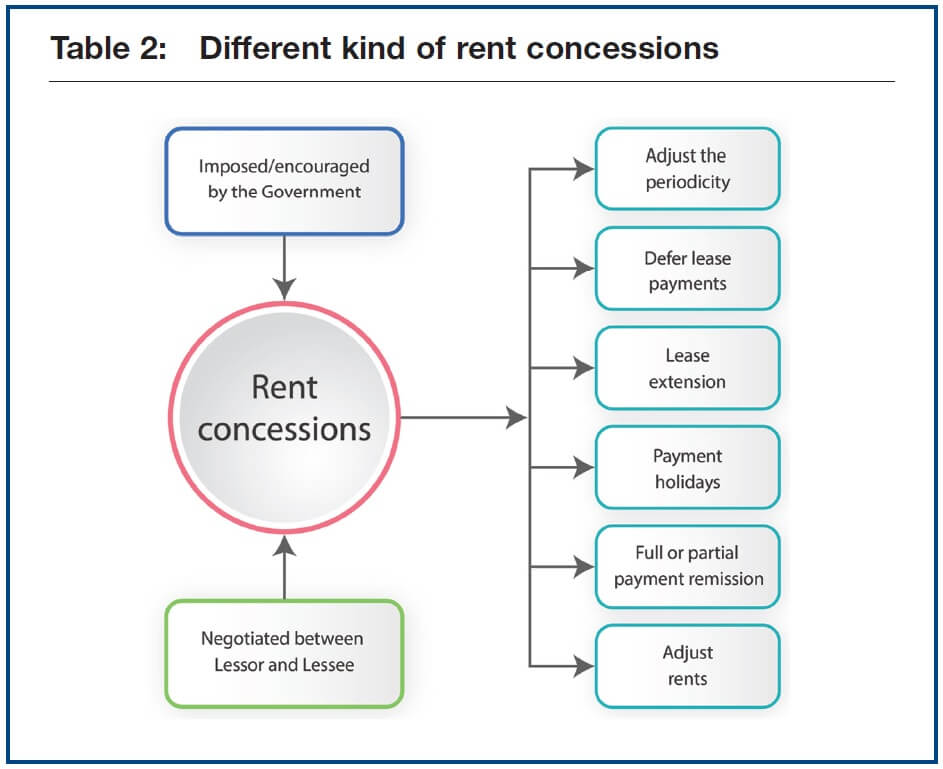

Following the different government actions and mass lease amendments which have been implemented and requested, sev- eral legal issues arise for leasing and credit businesses from the lessor’s/borrower’s point of view and from the lessee’s/customer’s point of view. Companies/banks reporting under IFRS have to translate those effects as well as the mitigated governmental meas- ures into accounting numbers and pertinent disclosures.

The IASB issued Covid-19-Related Rent Concessions (Amendment to IFRS16) on May 28, 2020. The project was set up to provide practical relief to lessees and rent concessions as a result of the Covid-19 pandemic.

For lessees: Lease accounting treatment for rent conces- sions. Following the rent concessions agreed between lessees and lessors that are imposed or encouraged by the government, we need to evaluate and determine the right accounting treatment under the new standards: whether rent concessions should be considered a contract modification or a non-contract modifica- tion. If the rent concession is considered a contract modification, then the lease liability for lessees will have to be recomputed using the IBR (Incremental Borrowing Rate) based on the mod- ification.

Rent concessions that lead to contract modifications. The IFRS 16-44 standard requires to consider a lease amendment as a separate contract if both criteria are met:

- “An increase in the scope of the lease by adding the right to use one or more underlying assets;

- and the consideration for the lease increases by an amount commen- surate with the stand-alone price for the increase in scope and any appropriate adjustments to that stand-alone price to reflect the cir- cumstances of the particular contract.” (IFRS 16, Annexes 2).

The IFRS 16-45 standard requires the lessee to:

- Recalculate the new discount rate for the remaining duration.

- Revise the lease liability to take into account this new discount rate and the revised payments.

- Revise the right-of-use asset amount.

All this in case a change in the consideration has led to the contract modification (including rent concessions).

Rent concessions with no contract modification. According to the IFRS 16-40 standard, a revaluation or an exercise of termi- nation options or extension (IFRS 16-20&21) is not considered a contract modification.

According to the IFRS 16-42 standard, a change in future payments resulting from an index or from rates changes (for example, the market rental rate change), and/or a change in the expected amounts payable under a residual value guarantee is not considered a contract modification.

According to the IFRS 16-38 standard, a variable lease pay- ment should be recognised in profit or loss. Rent concessions are considered a (negative) variable payment.

According to the IFRS 9-3.3.1 standard, a derecognition of the lease liability is required if the lease modification (including rent concession) would result in a partial extinction of the obliga- tion specified in the contract.

Right-of-use asset impairments. The IFRS 16.46(a) standard requires to decrease the right-of-use of the asset and lease liability and to recognise in the profit-and-loss account any gain or loss resulting from the lease modification, if the lease modification decreases the scope of a lease.

The huge number of lease modifications, including the rent concessions stemming from the Covid-19 pandemic, will prob- ably quickly impact asset values (especially concerning real estate).

It is necessary to have a close and detailed monitoring of fluctuating values and potential impairments.

It will also be necessary to increase the asset valuation fre- quency and to take into account the various asset valuation con- siderations in order to reduce this risk.

From the lessor’s point of view. (According to the Covid-19 considerations on the preparation of the half-year report 2020 under IFRS Brussels IFRS Centre of Excellence May 14, 2020.)1

The Board did not consider any amendment to lessor accounting.There is not any practical expedient planned by IASB for changes regarding lessors.

For most lessors with a large volume of lease contracts, this is their core business for which they would have processes and sys- tems in place that would allow them to manage any contract modification.

Table 3 shows us the current IFRS 16 as applicable for lessors.

How can a Covid-19 event be considered by IFRS 9 impair- ments? IFRS 9 principles are applicable to financial assets. Table 4 summarises the principles of the IFRS 9.

ECL: Expected Credit Loss. Following the Covid-19 pan- demic, the interruption of regular business operations has led to a huge number of customer rental inquiries. Lessors have been obliged to reconsider rental concessions rules and defer payments, and have faced a lack of liquidity.

This has a direct impact on the IFRS 9 staging and calcula- tion and the recognition of IFRS 9 impairment:

- Several assets will probably move from stage 1 to stage 2/3 but not all: only the ones that result in an increase in ECL.

- More assets will default, resulting in an increase in ECL.

The IFRB has published the different changes to take into account in IFRS 9, with the main changes listed below:

- Increase the number of potential scenarios included in ECL in order to take into account the effect of Covid-19, with the respective probability weightings.

- ‘Overlays’ will probably need to be added in order to readjust the amounts automatically calculated by the system within a short period of time.

- Impact the ECL measurement.

- New PD (Probability of Default) recalculation will need to be added based on the customer’s business.

Different effects of Covid-19 should be considered in the ECL. Table 4 illustrates the global consideration that should be taken into account.

Modelling the effects of Covid-19 will be very challenging. Companies should do their best to determine the effects and adjust the modelling techniques.

Companies need to evolve a lot in this respect in order to enhance risk management and preview solutions for the foresee- able future. This includes making significant changes to the cur- rent risk strategy so that it can remain profitable and limit the impact on ECL and on the deterioration of their risk classifica- tion. This consists of:

- Adding new guarantees or putting into place new agree- ments by managing private funding guarantees.

- Adding new mandatory insurances.

- Increasing risk sharing by using new kinds of securitisations or by using syndicated loans.

- Varying the types of assets.

How can the leasing software system be part of the cure, with a ‘Crisis mode’ or ‘COV in Bank’ management that can easily be switched on? It is clear that IT software should be at the heart of any leasing or lending company’s strategy to face the upcoming chal- lenges, given the multiple changes in this unclear economic situation.

Leasing software should have a robust product definition and pricing module that can easily be para- metrised to adapt the offers to any changes in the customer’s circum- stances or needs and provide intelli- gent offers with:

- grace periods, and franchise options;

- seasonable payment schedule;

- indexed rents and services;

- possible voluntary payments;

- automatic extensions or residual value financing;

- participation and subsidies from the government, from ven- dors or from other third parties;

- mandatory insurances and third-party guarantees.

Companies’ leasing models should evolve to increase profit and minimise risk. Leasing software can manage:

- Funding partner agreements with other financial companies to manage easily any risk sharing.

- The securitisation that can easily be switched on in case of a shortage or lack of liquidity.

- Agreements with the vendor/broker/supplier/guarantor/ participant/service provider/insurer to increase opportuni- ties and the percentage of penetration in the market. With those agreements it is possible to customise:

- financing products: the type of contracts that can be supported by this agreement;

- the pricing template using an interest matrix that can be fixed or variable or based on an index;

- the commission agreement, by offering more possible commission as shared income after extension;

- the participation settings in order to encourage vendors to sell their products and come up with attractive offers with reduced interest;

- multiple types of guarantee agreements, such as funding guarantee agreements that can also be remunerated;

- the purchase options commitment by offering commis- sions in case of releasing the asset.

- A robust scoring module with multiple types of scoring that can easily be set up taking into account different economic scenarios, such as setting ‘Crisis Mode’ or ‘COV in Bank’ type of scoring that can easily be switched on in case the sit- uation changes.

- A fully parametrised process to make fully automatic as many processes as possible, by using e-contracts, e-signature, inte- grated telephony/telephony/sms.

- An integrated risk management module to be able to calcu- late in real time the risk staging, and to take into account the current real-time situation using a simple setting in order to avoid going from stage 1 to stage 2/3 impacted by the Covid-19 crisis, and take into account the possibility to come back quickly to the normal situation.

- Intelligent risk modelling using AI to include easily different scenarios in the PD, ECL calculation.

Fortunately, such software packages exist, such as iMX Leasing for example. There are not very many, but they are avail- able, and they constantly acquire richer and stronger features through sustained heavy investment over the years by their respective editors. We do encourage you to investigate how the iMX Leasing solution can address the issues covered in this article in the specific context of your company and the challenges it faces.

In the final analysis, we all pursue the same goals: minimising the negative impact of the (post) Covid-19 calamity, and making sure leasing businesses emerge even stronger thanks to all the techniques and tools that have been implemented to mitigate the effects of the crisis.

Note:

1 https://www.iasplus.com/en/publications/global/ifrs-in-focus/2020/coronavirus

This article was published in the World Leasing Yearbook 2021.